While sustainability is firmly on the corporate agenda, many organisations are still struggling to translate intent into action, particularly at board level, where decisions about strategy, risk and long-term value creation are made. In March, Trialogue held a webinar exploring how organisations can meaningfully embed sustainability across strategy, governance, processes, metrics and performance management and reporting.

The panellists were Loshni Naidoo (Chief Sustainability Officer, JSE), Ayanda Seboni (Group Executive Mutuality, PPS), Carolynn Chalmers (Chief Executive Officer, Good Governance Academy) and Nick Rockey (Managing Director, Trialogue).

The session was moderated by Tina Playne, Head of Sustainability & ESG Advisory at Trialogue.

Why sustainability matters

ESG has come under political pressure recently, and ‘green-hushing’ where companies communicate less about sustainability – has become a phenomenon. But social and environmental pressures continue to build, so organisations can’t afford to retreat from sustainability commitments.

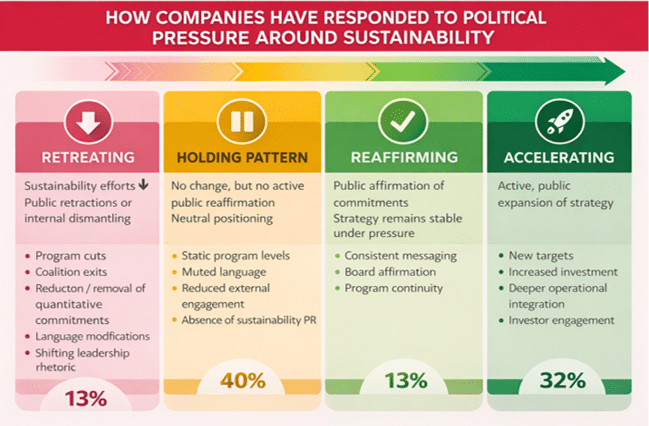

A 2025 observational mixed-method study conducted by Harvard Business Review found that only 13% of companies surveyed reported retreating from sustainability efforts, while 32% were accelerating, 13% were reaffirming, and 40% were essentially making no change (see Figure 1 below).

While ‘green-hushing’ reduced short-term risk, it may also weaken collective momentum, Playne told webinar attendees. “The message for executives is clear: you need to understand the shifting landscape, resist performative retreat, and recommit to visible, collaborative sustainability. Silence may be safe today, but only integrated action will create a competitive advantage.”

Figure 1: Findings from Harvard Business Review, as presented in Trialogue’s webinar.

Trialogue’s Integrated Sustainability Model

Playne referenced Trialogue’s Integrated Sustainability Model, which is built around five pillars:

- Pillar 1: Sustainability ambition

- Pillar 2: Leadership and governance

- Pillar 3: Systems and processes

- Pillar 4: Performance metrics and monitoring

- Pillar 5: Communication and messaging

The model helps organisations assess how well sustainability is embedded across the business and where gaps remain between strategy and execution. Reporting is an outcome of this integration: when purpose, strategy, governance and operations are aligned, sustainability moves from intent to measurable long-term value creation.

A shift to organisational urgency

Chalmers noted a shift from value-driven arguments – sustainability as “the right thing to do” – to a more urgent framing that notes the effect of ESG issues on company financial stability. South Africa is in a strong position due to our long history of integrated reporting and strong culture of voluntary disclosure. However, reporting is just one aspect of the broader – and shifting – sustainability landscape.

Naidoo noted that many large, listed companies in South Africa have already embedded sustainability at the board level, where it forms part of enterprise risk management discussions. Climate scenario analysis, in particular, is increasingly being driven by Enterprise Risk Management teams, although sectoral differences remain, especially where nature-related risks are more material to certain industries.

Seboni noted that collective action played a critical role in addressing the ozone depletion crisis in the 1980s and emphasised that sustainability requires both top-down leadership and bottom-up execution. While governments and international bodies play a role, adherence and implementation ultimately happen at the organisational and local level. Business leaders, she argued, shape the culture that determines whether sustainability commitments translate into action.

Boards and the governance gap

According to Chalmers, some boards are integrating sustainability into strategy, while others leave this largely to executive teams. “We’re not as compliant-driven from a Companies Act perspective,” she noted. “King V and corporate governance have emphasised sustainability and value creation a lot more.”

She described a “bell curve” of maturity: few boards treat sustainability as a core strategic driver, but few rely purely on compliance either. Most fall somewhere in between, with executive teams often ahead of boards in embedding sustainability-related financial considerations into strategy. On the African continent, however, Nigeria, Zimbabwe and Egypt have been the first to adopt sustainability-related financial disclosures.

Naidoo reinforced this with data from JustShare research showing that 55% of the JSE Top 40 boards lack a director with a sustainability-related qualification, while only 5% of directorships have this. “Ongoing capacity building for boards is a critical enabler for embedding sustainability in organisations,” she stressed, noting that many board members “don’t ask questions” because they fear exposing gaps in their knowledge. As a result, very little is debated.

Seboni added that governance models can also influence how sustainability is embedded at board level. At PPS, the mutual model removes the tension between shareholders and clients. Mutuals have members, not shareholders, and board members are elected from among the members themselves. Without shareholder pressure or external borrowing, long-term thinking becomes central to decision-making.

“In the boardroom, the biggest discussion that takes place is about intergenerational fairness – whether decisions made today will be fair for future generations,” she said, adding that PPS doesn’t borrow as it doesn’t have shareholders, so strategy needs to be long-term ensure inter-generational fairness. “Sustainability is baked into the model and has to be at the core,” she noted.

Trade-offs and long-term value creation

Panellists discussed navigating trade-offs between short-term financial pressures and long-term sustainability risks.

Chalmers noted that traditional risk reporting often presents a two-dimensional view, failing to distinguish between short‑, medium‑ and long-term impacts. As a result, boards tend to focus on the next financial year or two, even when risks require action decades in advance. Water scarcity, for example, is a case in point.

A stronger value‑creation lens, grounded in organisational purpose and stakeholder impact, is needed before sustainability is reduced to disclosure. Questions about who benefits and bears the costs, and how value is created or eroded, should inform strategy upfront, not be added at the reporting stage. “We’ve built this into corporate governance standard ISO 37000, where value generation is a key consideration for boards of directors,” Chalmers said, noting that the standard was “ahead of its time”.

The panellists agreed that organisations that integrate sustainability into strategy, risk and performance management will increasingly unlock a competitive advantage. Chalmers argued that this ultimately comes down to board behaviour and intent. Boards must decide whether sustainability is something to be minimised, optimised, or leveraged strategically, and set the tone accordingly through the questions they ask, the information they scrutinise and the trade-offs they are willing to confront.

Making the business case for sustainability

To secure board buy-in, financial considerations are important but not the whole story, said Seboni. At PPS, proposals are first assessed for financial implications, but decisions are framed with a future-oriented mindset.

She illustrated this with an example from the medical indemnity insurance market, where soaring premiums had left some professions, particularly gynaecology, close to unviable. However, for the good of society, walking away from this “distressed” class of insurance was not an option, so PPS took a long-term view despite underwriting risk.

By focusing on indemnity cover for health professionals and partnering with a US insurer, the organisation re-engineered the business model. “We turned a profit three years ago,” Seboni said, noting that business risk looked at with a sustainability lens can be turned into an opportunity.

Sustainability reporting: compliance today, value tomorrow

Naidoo explained that, for many organisations, engagement with new disclosure standards is still driven largely by obligation rather than strategy.

Turning to sustainability reporting, Loshni Naidoo noted that ongoing engagement by the Companies and Intellectual Property Commission (CIPC) and the Department of Trade, Industry and Competition (DTIC) around the IFRS Foundation’s ISSB sustainability standards – IFRS S1 and IFRS S2 – has raised widespread questions across the market, affecting not only listed companies but also SMMEs, state-owned entities and other organisations operating in South Africa.

Companies are trying to understand why these standards are being introduced, which companies will be affected, how they align with King V, double materiality and integrated reporting, and how to implement them in practice. Many organisations are accustomed to Global Reporting Initiative (GRI)-based systems, while the SASB Standards and the newer IFRS S1 and S2 disclosure standards are still bedding down in practice, raising practical concerns around systems, data management and application.

Naidoo acknowledged that most companies will begin this journey with a compliance mindset – they need to “tick the box no matter what”. However, she expects this to shift over time as organisations begin to see the value of the information.

“We’re not just asking questions about compliance, but about how we embed sustainability into strategy, risk and so on,” she said. “I hope that focus continues, and that we don’t lose sight of the bigger picture. What we want is a specific, sustainable outcome – not just an output – from this process.”

She also urged companies to engage when the DTIC and the CIPC put out consultations or requests for comment, as this is “in the best interests of our economy and our region”.

Accountability, behaviour and the role of the board

As sustainability disclosures expand, questions of accountability – particularly at the board level – are becoming more prominent. Chalmers argued that the starting point is not regulation, but behaviour. When advising boards, she first asks directors to reflect on their own approach: whether they intend to do the minimum, do their best, or optimise. That choice, she said, shapes whether sustainability becomes embedded or becomes a repetitive compliance exercise at the end of each reporting cycle.

Boards set the tone through the questions they ask and the information they choose to interrogate. Too often, sustainability disclosures are “taken as read” once they have been signed off, rather than examined through a strategic lens.

She noted that many boards are operating in survival mode, focused on running the business, rather than on the business of governing. Integrated reporting exposes this clearly: some reports are genuinely interrogated and reflect the board’s voice and attitude; others are treated as a tick-box exercise. Boards face a choice about the level at which they want to govern – whether integrated reporting is owned as an expression of board intent and values, or reduced to another compliance task.

Seboni added that behaviour change is unlikely without the right incentives. One of the most effective levers, she argued, is remuneration. At PPS, sustainability is one of eight strategic pillars contributing to organisational performance, supported by a cross-functional execution team of senior leaders.

While sustainability is not yet embedded in every individual scorecard, it is firmly positioned as a strategic initiative with senior leadership accountability. This, Seboni noted, sends a clear signal that sustainability is not peripheral, but integral to how performance is measured and managed.

What distinguishes organisations that truly embed sustainability?

Asked to distil the difference between organisations that embed sustainability and those that merely talk about it, Naidoo pointed to the ability to balance two time horizons at once: the backwards-looking nature of short-term financial reporting and the forward-looking perspective required by sustainability. Organisations that can hold both views simultaneously, she argued, are better positioned to unlock competitiveness, opportunity and long-term value creation.

Rockey argued that embedding sustainability is fundamentally a board-level mandate and values issue, not a technical reporting exercise. “You can’t empower the organisation to drive change unless the mandate comes from the board,” he said, adding that this takes time, effort and sustained commitment.

Many boards remain poorly sensitised to ecological considerations, he said, with governance still dominated by financial and accounting perspectives. As a result, most organisations are “muddling along”, with only a small group truly shifting towards holistic value creation. “The organisations that really create value are still on the fringe of the bell curve – they’re the exception, not the rule,” he said. Sustainability, he argued, is too often framed defensively as risk management rather than through a clear understanding of the trade-offs that materially affect supply chains, production, and services. “You can have all the rules in the world, but if executives are chasing a bonus cheque, they’ll optimise for that,” he pointed out.

Ultimately, he emphasised that value creation must be embedded in strategy. “The real trade-offs are not resolved through frameworks or diagrams, but through debate in the boardroom,” he said. “What matters most is a clear understanding of what is material to the organisation, informed by meaningful engagement with stakeholders.”

He concluded that organisations that truly embed sustainability over time will be distinguished by their values, their willingness to confront difficult trade-offs, and the depth of their board-level decision-making.

The cost of doing business will rise without a sustainability focus

The panellists agreed that market forces, consumer expectations and technology will increasingly expose poor practice. Seboni warned that the price of doing business will rise for organisations that fail to act. Leadership, she argued, will ultimately make the difference, reinforced by growing peer pressure within business.

Chalmers pointed to emerging efforts to translate sustainability into management systems, including the Good Governance Academy’s ESG Exchange, developed in collaboration with the Pan‑African Federation of Accountants. She expressed confidence in the South African and African context as communities have repeatedly demonstrated their ability to respond quickly and pragmatically, from energy solutions during load shedding to collective action during water crises.

As Africa’s population grows and climate impacts deepen, organisations that embed sustainability into strategy and governance will be better positioned to adapt, even if the performance gap is wider in developed markets.

Find out more

- Explore the Integrated thinking and ESG topic on the Trialogue Knowledge Hub.

- Complete Trialogue’s Sustainable Business Self-Assessment, a practical, executive-level diagnostic tool that helps organisations move from sustainability intent to embedment.